Social belief in democratic establishments impacts the flexibility of these establishments to hold out coverage. In new analysis, Rustam Jamilov reveals how lowering belief within the U.S. establishments has lowered the flexibility of the Federal Reserve to affect the financial system in states that exhibit decrease ranges of belief.

Belief in establishments can form the best way people and companies react to adjustments in financial coverage. Lack of belief hampers the flexibility of the central financial institution to have an effect on the financial system, even within the quick run. Institutional credibility and integrity—particularly in a world of rising populism—are vital for financial coverage effectiveness. For instance, distrustful brokers could underreact to financial coverage bulletins or query the financial authority’s dedication to its mandate.

Belief in establishments has been declining in the USA for many years (Determine 1). This pattern is extraordinarily regarding as a result of generalized belief is an integral part of a networked society. It encompasses civicness and transactional reciprocity, which in flip allow the society to operate successfully. The affect of belief—or social capital—on elementary financial forces, starting from progress and growth to monetary market participation, has been properly documented. In high-level coverage circles, analysis on belief is turning into more and more integral for knowledgeable authorities laws.

Determine 1: A Disaster of Belief

Notice: Responses to the survey query “Do you will have confidence in congress?” Determine is from Part 1 of Jamilov (2023). Unique knowledge is from the Basic Social Survey.

The connection between belief and central banking, nonetheless, stays poorly understood. What’s the affect of belief on financial policymaking? Has the collapse of belief diminished financial coverage effectiveness? In a brand new paper, I doc that U.S. states with excessive ranges of belief in establishments are systematically extra conscious of adjustments in financial coverage. Together with a easy behavioral New Keynesian mannequin, I conjecture that the secular decline in belief could have contributed to a big discount within the means of the Federal Reserve to affect the financial system. My findings warn that crises of belief might result in crises of coverage inefficacy.

My empirical strategy builds on the burgeoning empirical literature that exploits spatial variation for identification. I start by measuring regional variation in belief with geo-coded survey-based indicators from the sixth wave of the World Values Survey (WVS). Surveys have been proven to be a helpful measurement software for the research of data rigidities, the pass-through of coverage interventions, and elicitation of first-order social considerations. For our functions, we concentrate on 20 questions that attempt to elicit belief and confidence in establishments. These questions ask the respondents to judge their confidence within the authorities, parliament, banks, main corporations, and so on.

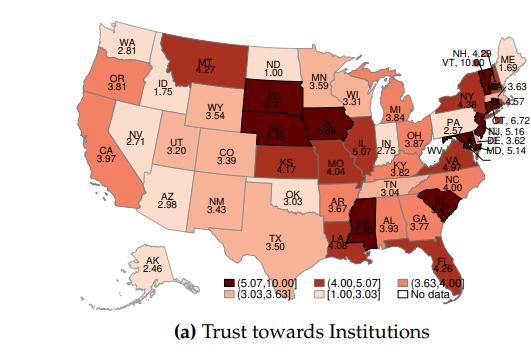

Determine 2: The Geography of Belief in Establishments

Notice: This determine reveals regional variation within the indicator of belief in establishments. Numbers have been scaled to lie within the [1,10] interval the place 1 signifies low belief and 10 signifies excessive belief. The District of Columbia and Hawaii usually are not proven. Particulars on index development are in Part 2 of Jamilov (2023). Unique knowledge is from the World Values Survey.

I then took the best-fit line of the weighted averages of particular person survey responses on the state degree to assemble the baseline, low-dimension, state-level measure of institutional belief: TrustInstitutions. Determine 2 plots the regional distribution of TrustInstitutions. One can see wealthy heterogeneity in institutional belief, starting from low-trust states like North Dakota, Idaho, and Alaska to high-trust states like Vermont, Connecticut, and Nebraska.

The primary empirical take a look at consists of two easy steps. First, I run quarterly state-level regressions (native projections) of native actual GDP progress on the financial coverage shock. Particularly, the shock represents a contraction that ought to result in a decline in financial efficiency. In Step 2, I run a cross-sectional regression of the estimated coefficients on our fundamental variable TrustInstitutions and extra controls. A unfavourable and statistically important estimate in Step 2 would imply that states with larger ranges of native belief in establishments are extra conscious of the financial coverage contraction, i.e. their native GDP progress slows down by extra.

Naturally, the connection between our regional belief measure TrustInstitutions and financial coverage might be influenced by quite a lot of different variables. I subsequently assemble a big array of socio-economic, demographic, and behavioral controls that might be correlated with the spatial distribution of belief. To ease the dialogue, I’ve grouped all of the controls by theme. The total checklist of themes that I’ve managed for contains social preferences (e.g. danger aversion), native macroeconomic power, demographics, schooling, political opinions and liberalism, consideration to inflation, populism depth, wealth inequality, authorized variations, inventory market wealth, immigration aversion, religiosity, the scars of slavery (native slave to inhabitants ratio from the 1860 U.S. Census), the China syndrome, inventory market participation, monetary literacy, urbanization fee, coal manufacturing, banking entry, and the Putnam (2000) and Alesina and La Ferrara (2002) present social capital indices.

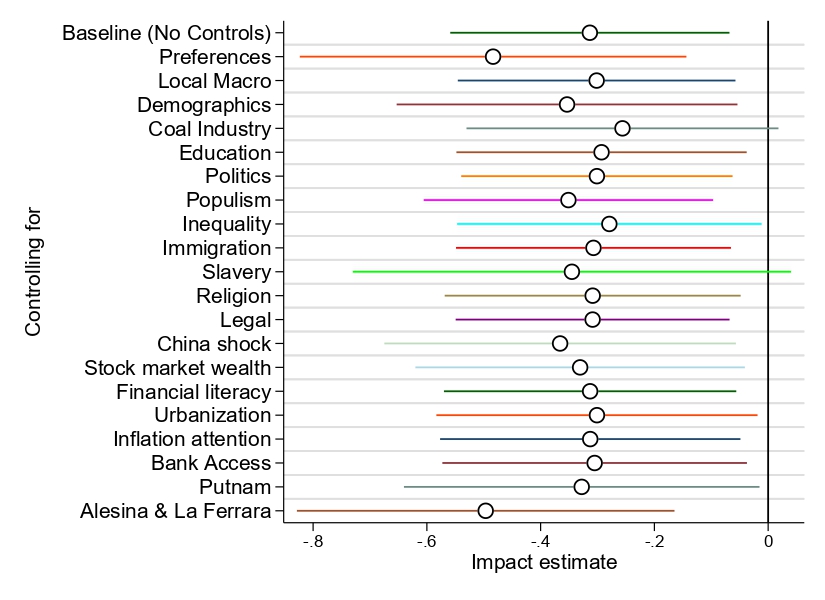

Determine 3: Belief and Financial Coverage

Notice: This determine presents outcomes from a two-step empirical process detailed in Part 2 of Jamilov (2023). The determine plots level estimates and 90% confidence bands from this step. The primary row represents the baseline specification with no further controls. Every subsequent row states which set of controls has been added to the baseline specification.

Determine 3 studies a key results of the research. The primary row represents the baseline specification from Step 2 with no further controls. Every subsequent row states which set of controls has been added to the baseline specification. Throughout the board, we observe unfavourable and statistically important coefficients, i.e., TrustInstitutions continues to be statistically significant even after making an allowance for further management variables. Recall that the underlying financial shock is a contraction. A unfavourable estimate within the determine subsequently implies that following financial contractions native GDP progress is extra unfavourable in states with excessive ranges of belief in establishments. In different phrases, financial coverage is stronger in high-trust areas. This result’s strong to virtually all different channels of causality. The one regional attribute that seems to be related is the “Slavery” indicator. The legacy of slavery might have left unhealed scars within the psyche of the inhabitants: excessive historic slavery depth could have contributed to decrease belief in current instances. Extra analysis is required on the racial origins of modern-day mistrust, political cleavages, and coverage effectiveness.

We now revisit Determine 1 and attempt to reply the next query: has the rise of mistrust in the direction of establishments made U.S. financial coverage much less efficient over time? To this finish, I construct a easy New Keynesian framework with one behavioral friction: brokers don’t react absolutely to rate of interest actions however exhibit mistrust. Within the mannequin—as within the knowledge—when belief is low, brokers pay much less consideration to the financial policymaker and underreact, i.e. financial coverage is much less efficient. The query is: by how a lot? A key parameter that governs mistrust within the mannequin is calibrated to match the noticed enhance within the share of respondents that reply with “Hardly Any” to the query “Do you will have confidence in congress?” The calibrated and solved mannequin predicts that the long-run (i.e. after 20 quarters) macroeconomic response to the identical financial coverage shock is 20% milder in 2023 than what it was in 1990, every thing else equal. In fact, the framework could be very stylized and introduces only one departure from the usual mannequin, whereas the U.S. financial system has gone by many, multi-dimensional adjustments over the identical 1990-2023 interval. In a richer mannequin, the 20% quantity might be decrease. Extra theoretical work is required to quantify the macroeconomic results of belief and social capital.

Whereas my research has stuffed some gaps, much more work must be completed to refine the social capital channel of financial policy-making. First, populism is ravaging throughout the Western hemisphere and the rise of populism goes hand in hand with a disaster of belief. My research can communicate on this subject by conjecturing that populism can probably have an effect on central banking independence, efficiency, and conduct by an interplay with the institutional belief capital inventory. Extra quasi-experimental work on this course is required. Second, firm- degree surveys can probably elicit companies’ amount and pricing plans conditional on randomly offered (by the econometrician) coverage forecasts – a type of an institutional “belief stress take a look at.” Such assessments may be carried out by regulators regularly.

Articles characterize the opinions of their writers, not essentially these of the College of Chicago, the Sales space College of Enterprise, or its college.

Originally posted 2023-06-26 10:00:00.