Are the antitrust enforcement businesses in the USA sufficiently stringent in difficult mergers? In a brand new working paper, Vivek Bhattacharya, Gastón Illanes, and David Stillerman inform this debate by inspecting the value and amount results of U.S. retail mergers and modeling the implications of other antitrust regimes.

Has antitrust coverage in the USA been too lax? It is a matter of great debate between lecturers, business individuals, and policymakers. Answering this query requires a scientific evaluation of what results accomplished mergers have had within the U.S. and a prediction of how these results would change below various antitrust regimes. In a brand new NBER working paper, we offer proof on each these points.

We discover that U.S. retail mergers elevate costs by 1.5% and reduce portions offered by 2.3%, on common, however there may be substantial heterogeneity in these results. 1 / 4 of mergers lower costs by at the least 5.1%, whereas one other quarter enhance costs by at the least 5.8%. Utilizing the noticed merger results and a mannequin of antitrust enforcement, we estimate that, on common, U.S. antitrust businesses (the Division of Justice Antitrust Division and the Federal Commerce Fee) block mergers which might be anticipated to lift costs by between 8-9%. At this threshold, many anticompetitive mergers are allowed to proceed whereas procompetitive mergers are hardly ever blocked. We discover that tightening the edge of enforcement can cut back the likelihood that anticompetitive mergers are accredited with out a big change within the likelihood of procompetitive mergers being blocked. That mentioned, the variety of circumstances challenged by the antitrust enforcement businesses would enhance, suggesting that tightening requirements shouldn’t be with out price.

What have mergers finished?

Retrospective evaluation of mergers is ceaselessly topic to 2 types of choice bias. First, mergers chosen for evaluation are sometimes these of specific curiosity to researchers or to policymakers, that means these mergers might not be consultant of all consummated mergers. Second, offers that had been studied should have been accredited by the antitrust enforcement businesses and thus might not be consultant of the kinds of mergers accredited in alternate antitrust regimes. Our evaluation tackles each these sources of bias. We analyze all (sufficiently giant) mergers in client packaged items merchandise in the united statesfrom 2006-2017, which ensures that our pattern is consultant of mergers in a single business. We then develop an financial mannequin to research choice into merger approval and predict outcomes in alternate antitrust regimes.

We use knowledge from NielsenIQ, which offer weekly costs and portions on the product degree for a big set of shops. We then use SDC Platinum, a complete dataset of M&A exercise within the U.S., to determine all transactions with deal sizes bigger than $280 million involving merchandise prone to be offered within the shops in our dataset. This consists of firms that promote meals, electronics, cosmetics, and prescribed drugs. Every deal entails firms that will compete in a number of product markets: Conglomerate A and Conglomerate B could each promote pickles and ketchup, for instance. We deal with every product market of a deal wherein the 2 events each offered merchandise earlier than the transaction as a separate merger. We finish with a pattern of 126 mergers coming from 50 separate offers.

In our baseline specification, we estimate the mergers results utilizing a before-after comparability of costs illustrated in Determine 1. We use knowledge from the 2 years earlier than the completion date of the merger to estimate (i) a brand-specific time development, (ii) seasonality results, and (iii) UPC-geography-specific variations in value ranges. This permits us to foretell a “but-for” value for every product for every geography after the merger. The distinction within the noticed value and the but-for value, averaged throughout merchandise and geographies over the 2 years after the merger, is our estimate of the impact of the merger.

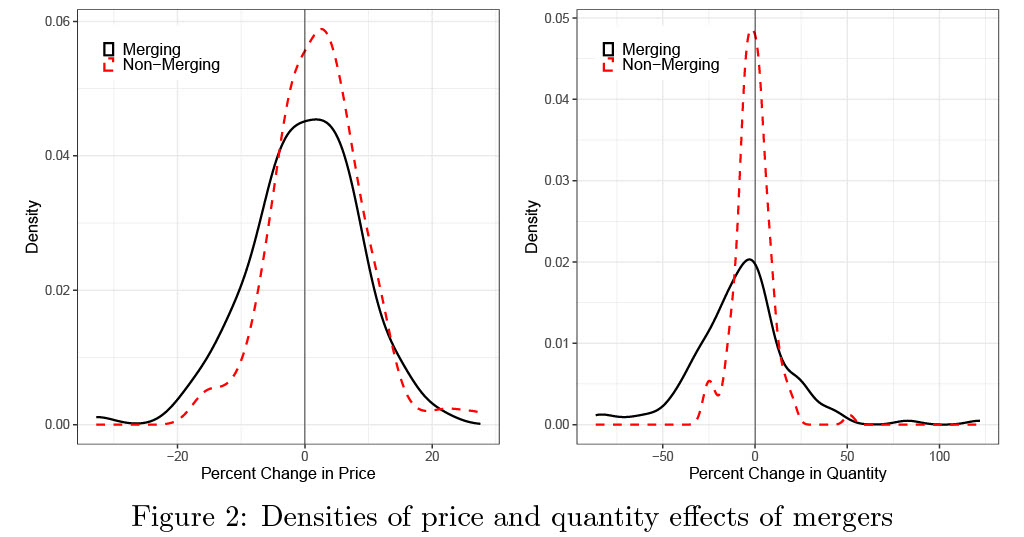

Determine 2 plots the distribution of value (left panel) and amount (proper panel) results of mergers individually for merging events and their opponents. The common value results of accomplished mergers are moderately modest: the imply change is -0.1% for merging events and a couple of.1% for non-merging events, equivalent to a 1.5% enhance total. This stands in distinction to estimates from meta-analyses of the literature, which discover common value will increase round 5-7%. The amount results are bigger. A placing discovering from our paper is that, on common, portions offered by merging events lower by 7.6%. The distribution in outcomes for non-merging events is far tighter.

Furthermore, there may be important heterogeneity within the outcomes of mergers: Over 25% of mergers result in a value lower for merging events of greater than 5.1%, and one other 25% result in a value enhance of greater than 5.8%. Related heterogeneity exists for the amount results. This heterogeneity performs an essential function in our evaluation of antitrust coverage, and it hints on the issue of the issue enforcement businesses face: mergers could be each considerably procompetitive (main to cost decreases) or considerably anticompetitive (main to cost will increase).

How do present pointers align with these results?

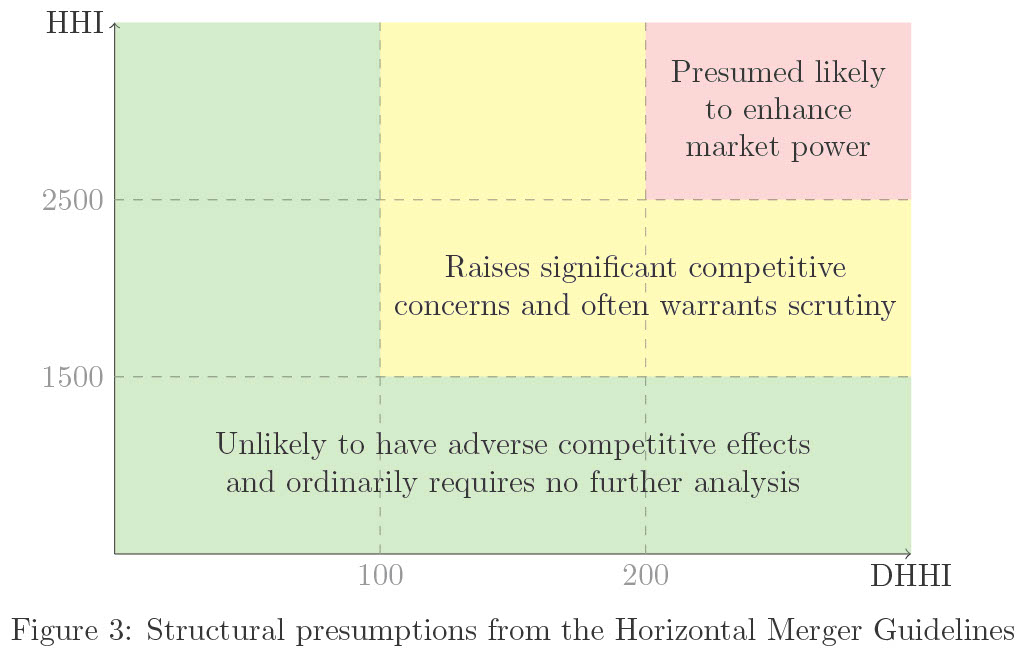

To help with the tough process of figuring out dangerous mergers, the Horizontal Merger Pointers codify the so-called “structural presumptions” the businesses use in conducting their assessments of whether or not a merger is anticompetitive. These presumptions use each the Herfindahl-Hirschman Index (HHI) of the merger—the sum of the squares of the market shares of firms available in the market—and the change within the HHI induced by the merger (DHHI).

Determine 3 exhibits the HHI and DHHI areas outlined within the 2010 revision of the Pointers together with the language used to explain every area. In July 2021, President Joe Biden issued an government order to revisit these Pointers, to which many economists submitted feedback, and these areas are anticipated to be reassessed.

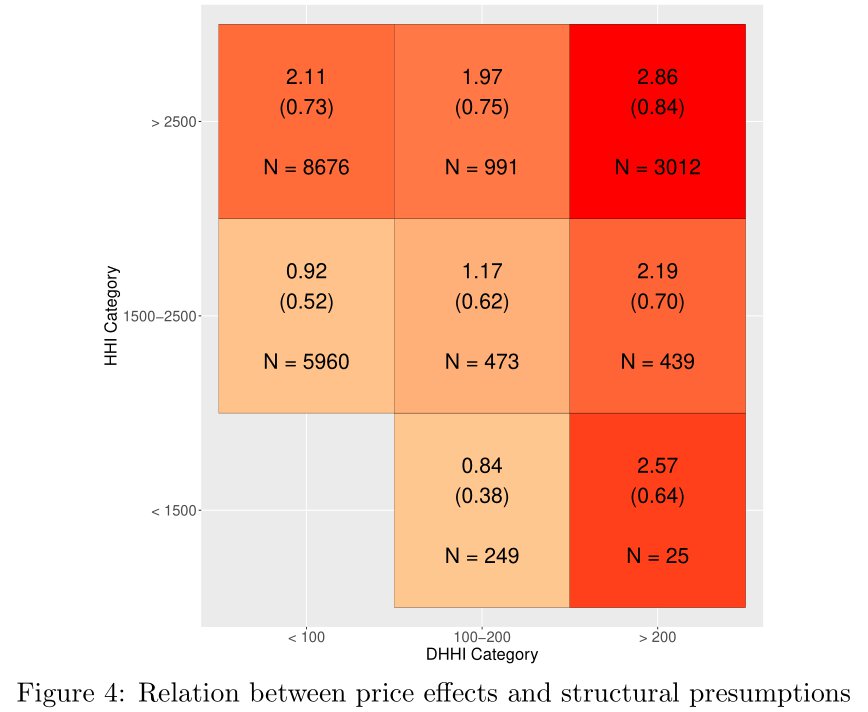

We correlate our estimated value modifications with market construction to judge the effectiveness of those structural presumptions in figuring out anticompetitive mergers. On the nationwide degree, we discover that DHHI is certainly associated to will increase in costs: mergers with DHHI between 100 and 200 have total value will increase which might be 2.9 proportion factors bigger than these with DHHI under 100, and people with DHHI above 200 are 5.1 proportion factors bigger.

Even when mergers don’t result in appreciable modifications in market construction nationally, they nonetheless could current aggressive considerations in a subset of geographic markets. We repeat our evaluation by estimating value modifications on the merger-geography degree and correlating these modifications with geography-level metrics for market construction. Determine 4 exhibits the distinction in costs for every bin of HHI-DHHI, relative to the bin the place HHI is lower than 1500 and DHHI is lower than 100, in a format that mirrors Determine 3. This evaluation controls for the general degree of value modifications in a merger utilizing a merger mounted impact. We discover that sometimes each bigger DHHI and HHI correlate with bigger value modifications, in keeping with the presumptions within the Pointers.

How would various antitrust coverage carry out?

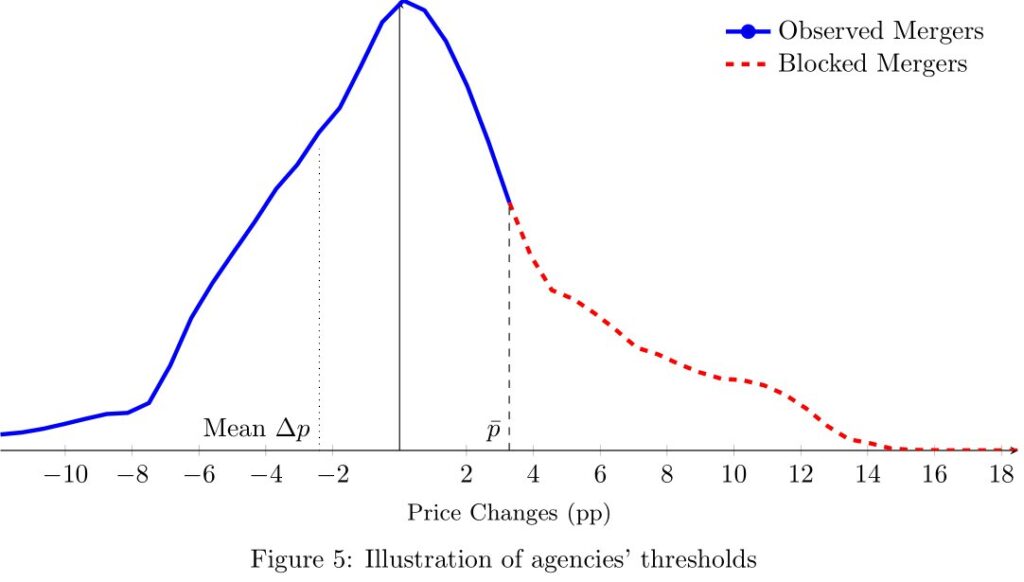

Discovering small common value modifications doesn’t imply that present antitrust coverage is strict. Determine 5, tailored from Carlton (2009), illustrates this level. The whole distribution (blue and crimson) corresponds to the value results of all potential mergers. Suppose that the businesses can predict the value change of a merger precisely and block all mergers with a value change bigger than p. Then, the businesses’ threshold could be p and, since we don’t observe any blocked mergers, the common value change estimated within the knowledge could be the common of the blue a part of the distribution (denoted Imply Δp).

Asking how strict antitrust enforcement is, on this mannequin, is tantamount to asking what p is. We estimate a extra life like model of the mannequin, permitting for businesses to have uncertainty over the value change {that a} merger will induce. To estimate each the edge and the uncertainty, we conduct the next thought experiment. Given the company has restricted assets, suppose that if it faces two mergers with an identical market constructions, however one among them occurs to be bigger by way of gross sales, it focuses its enforcement efforts on the bigger merger. If it challenges plenty of giant mergers, then it should have a strict threshold for these mergers. Now, if the realized value distribution of the big mergers which might be allowed by the company seems so much like the value distribution for the small mergers (which go largely unchallenged), then the company should have a loud sign of the value change a merger would induce. If the value modifications for giant mergers are smaller than the value modifications for small mergers, then the company should have a fairly exact estimate of value modifications and thus is ready to goal essentially the most dangerous mergers.

We formalize this mannequin mathematically and estimate it by connecting the estimated value modifications from above and enforcement actions by the DOJ and the FTC. For the needs of our evaluation, we take an enforcement motion to be both a divestiture or a grievance that leads the events to withdraw the merger. We discover that on common, the businesses goal to problem mergers that they count on will enhance costs by greater than 8-9%. We additionally discover that businesses have a reasonably exact sign of the value modifications induced by the merger.

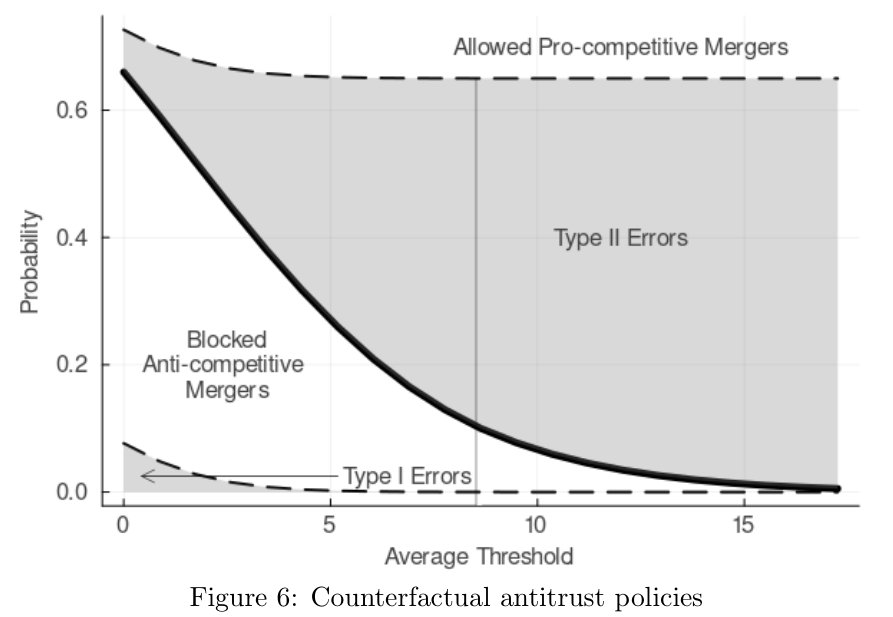

Determine 6 explores what this implies for various antitrust coverage by plotting the likelihood of a problem together with the chances of creating one among two kinds of errors: blocking procompetitive mergers (“sort I error”) or permitting anticompetitive mergers (“sort II error”). Companies enable mergers above the strong line and problem them under. We discover that shifting to a 5% value change threshold from the present one (marked by a vertical line) wouldn’t have a big impact on blocked procompetitive mergers and would considerably cut back the likelihood of permitting anticompetitive mergers. Nevertheless, it could nearly triple the variety of mergers the businesses must problem.

With these findings, we are able to return to the query with which we began the paper: is antitrust coverage too lax? On the present degree of stringency, many anticompetitive mergers undergo whereas primarily no procompetitive mergers are blocked. We discover that businesses may display screen out these mergers, however it could entail a major enhance of their workload.

Articles characterize the opinions of their writers, not essentially these of the College of Chicago, the Sales space College of Enterprise, or its school.

Originally posted 2023-07-03 10:00:00.