In new analysis, Enghin Atalay, Alan Sorensen, Christopher Sullivan, and Wanjia Zhu discover that mergers and acquisitions usually result in the merged agency providing much less product selection than when the 2 corporations operated pre-merger.

In 2022, mergers and acquisitions (M&A) in the US totaled $2.4 trillion. M&A supply buying corporations the distinctive alternative to leverage their managerial know-how over a wider set of product or geographic markets. On the similar time, the consolidation induced by M&A poses a perennial concern for policymakers relating to product worth, high quality, innovation, and, to be explored on this article, selection.

How corporations select their post-M&A product portfolios sheds gentle on the synergies and price reductions that mergers afford in addition to the potential harms to customers by lowered product availability. In response to one set of fashions, M&A afford merging corporations the chance to discontinue carefully competing merchandise in order to scale back expensive duplication and profit-reducing product market cannibalization. In response to others, M&A permit corporations to shortly scale up in sure product segments. As among the acquired product traces won’t align with the merged agency’s core competencies, these theories would predict substantial post-merger churn, with the merchandise which can be removed from the middle of the merged agency’s portfolio extra prone to be spun off or shuttered. Fashions inside this second set predict that buyers may have entry to a narrower vary of merchandise, and thus a decline in client surplus above and past greater costs that will consequence from the merger.

Earlier analysis gives proof in keeping with every of those factors of view. On the one hand, Vojislav Maksimovic, Gordon Phillips, and N.R. Prabhala doc that almost half of crops bought in manufacturing acquisitions are shut down or spun off inside the three years following the M&A with, crucially, crops in peripheral industries (i.e. these outdoors the agency’s core markets) considerably much less prone to be retained. Then again, of their analyses of mergers amongst radio broadcasters, Steven Berry and Joel Waldfogel and Andrew Sweeting discover a post-M&A improve in product selection.

In a brand new paper, we contemplate the evolution of merging corporations’ product portfolios in a pattern of 66 M&A amongst corporations within the client packaged items sector. As within the work of Maksimovic, Phillips, and Prabhala, our pattern attracts on all kinds of product markets. Just like the evaluation of Berry, Waldfogel and Sweeting, we contemplate the varieties that buyers have entry to, wanting inside detailed product markets. In our paper, we set up three foremost empirical patterns:

- First, merging corporations scale back the variety of merchandise they promote, with the results materializing one 12 months after the M&A and accelerating over the following a number of years.

- Second, merging corporations are inclined to drop and add merchandise on the periphery of their joint product portfolio.

- Third, the online impact is a rise within the similarity among the many merchandise that corporations supply following a merger or acquisition.

To reach at these outcomes, we assemble a pattern of mergers and acquisitions amongst client packaged items producers within the food-and-beverage trade. We determine M&A consummated between 2006 and 2019 utilizing the Securities Information Firm (SDC) Platinum Mergers and Acquisitions database. We deal with horizontal mergers involving corporations that produce a minimum of some comparable merchandise (e.g., a merger of two cereal producers versus a cereal and a frozen pizza producer) and for which the buying agency purchases a one hundred pc stake of the goal agency (or a subset of the goal agency’s traces of enterprise). Utilizing the NielsenIQ database—which, throughout our time interval, incorporates detailed data on merchandise bought in additional than 35,000 taking part grocery, drug, mass merchandiser, and different shops—we will then decide the set of merchandise provided by these corporations earlier than and after they merge. Our closing pattern contains 66 mergers and acquisitions, masking 361 M&A-by-product market pairs.

A key step in our evaluation of product portfolios is to outline the dissimilarity (“distance”) between any two merchandise in our dataset. We make use of two approaches, one which depends on abbreviated product descriptions offered by NielsenIQ, and an alternate that depends on buy patterns of particular person households whose purchases are tracked by NielsenIQ. Within the first strategy, two merchandise with a excessive fraction of the identical key phrases of their product descriptions are labeled as shut to 1 one other. Within the second, the similarity between two merchandise is predicated on how generally they’re bought by the identical family.

As an illustrative instance, contemplate Nestlé’s 2010 acquisition of Kraft’s frozen pizza manufacturers. Two of the acquirer’s (Nestlé’s) merchandise are Stouffer’s Deluxe French Bread Sausage, Pepperoni, Mushrooms and Onion Pizza and DiGiorno Skinny Crust 4-Cheese Pizza. The goal agency (Kraft) produced a Tombstone Authentic Deluxe Sausage, Pepper, Onion, and Mushroom Pizza. Our first product-description strategy would say the Tombstone pizza is nearer to the Stouffer’s pizza than to the DiGiorno pizza primarily based on the overlapping phrases “deluxe,” “sausage,” “mushrooms,” and “onions.” Additional, suppose that within the client panel, which tracks households over time, we observe that fifty p.c of the households that commonly buy the Tombstone pizza additionally buy the DiGiorno pizza a minimum of as soon as, whereas solely 5 p.c of those “Tombstone households” buy the Stouffer’s pizza. Our second household-purchase strategy would likewise conclude, straight from the customers’ conduct over time, that the Tombstone pizza is nearer to the Stouffer’s pizza.

Utilizing an occasion examine empirical methodology, we first examine the entire variety of merchandise provided by the merged corporations in our pattern as much as six years after the M&A to the mixed variety of merchandise provided by the merging corporations straight earlier than. Determine 1 plots modifications within the logarithm of the variety of merchandise on the firm-by-product-market stage across the time of every M&A.

Mergers are related to considerably fewer merchandise bought, however solely with a lag. (The red-dashed line and thin-solid-green line give, respectively, 90 and 95 p.c confidence intervals.) In response to Panel A of Determine 1, the variety of merchandise bought begins to fall about one 12 months after the M&A, accelerating thereafter. By 4 years after the M&A, the merging agency is promoting 40 p.c fewer merchandise.

These internet modifications are adverse each for merchandise initially bought by the buying agency and for these bought by the goal agency (in Panels B and C of Determine 1, respectively), however with considerably bigger results for these associated to the goal agency. Lastly, we discover that merging corporations’ product portfolios neither shrink nor develop within the 12 months and a half previous to the M&A.

The web discount within the variety of merchandise provided by merging corporations should be in keeping with both greater or decrease product selection. For instance, if the merging corporations remove many comparable merchandise to keep away from cannibalization whereas including just a few merchandise within the periphery of their product area, then selection will increase. As an alternative, if the merged agency predominately drops merchandise that are on the periphery of its portfolio whereas barely increasing its choices within the core, then selection decreases.

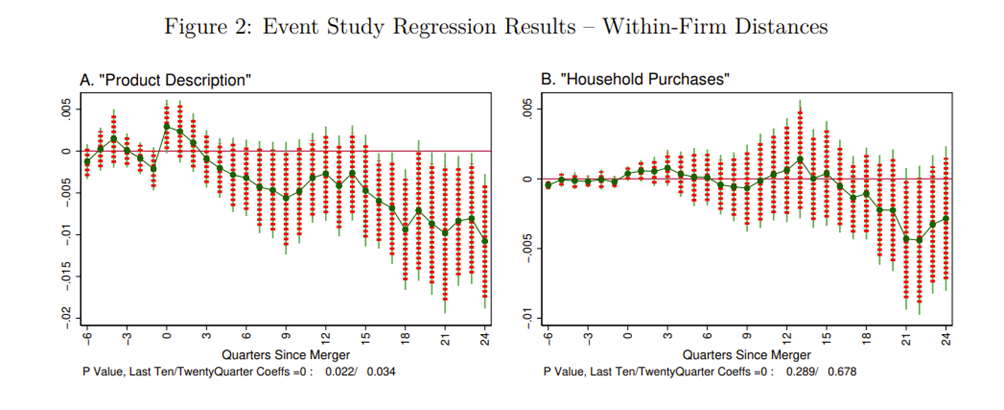

To differentiate between these two hypotheses, we discover how the general number of merchandise provided by the merging agency modifications. We first measure a agency’s product selection as the common of all of the pairwise distances amongst its merchandise inside a given product market, the place distance is measured both utilizing our product-description or household-purchase strategy. We then conduct an occasion examine evaluation to see how these measures of selection evolve within the 12 months and a half earlier than and 6 years after the merger.

Determine 2 plots modifications within the common pairwise distances for every firm-by-product-market pair. As in our evaluation of the variety of merchandise bought, we don’t discover any systematic change in common product similarity within the six quarters main as much as the M&A. As an alternative, the common distance inside merging-firm-by-product-market pair declines slowly and inconsistently over the primary six years after the M&A. The results we determine are modest but economically related: Panel A exhibits a 0.08 normal deviation discount in product selection (as measured with the “product description” metric) 18 to 24 quarters after the M&A. Panel B of Determine 2 exhibits a qualitatively comparable, however much less exactly estimated, relationship between M&A exercise and within-firm distances utilizing the “family buy” metric.

To unpack these outcomes additional, we contemplate the relative significance of newly showing and disappearing merchandise in explaining the general decline in selection. To take action, we estimate two units of logit regressions, one on the chance of a product being dropped inside 10 quarters of a merger and one on the chance of a product being newly added inside the similar interval. We estimate that merging corporations are inclined to each drop and add merchandise which can be removed from the middle of their joint product portfolio. (These relationships maintain each when contemplating the household-purchase- and the product-description-based notions of distance.) Since mergers are inclined to contain so many extra previous merchandise exiting the market than new merchandise coming into the market, on steadiness, mergers result in declining within-firm product distances.

After M&A, merging corporations promote fewer merchandise, with better product similarity among the many merchandise that they do promote. Taken collectively, our outcomes encourage analyzing post-merger product repositioning in particular person merger circumstances. Antitrust coverage carefully considers the affect of M&A on welfare, and even small modifications in corporations’ product portfolios could have substantial implications for client welfare.

Creator Word: Analysis outcomes and conclusions expressed are these of the authors and don’t essentially replicate the views of the Federal Reserve Financial institution of Philadelphia, the Federal Reserve System, or the Federal Reserve Board of Governors.

The researchers’ analyses had been calculated (or derived) primarily based partly on information from Nielsen Shopper LLC and advertising and marketing databases offered by the NielsenIQ Datasets on the Kilts Heart for Advertising Information Heart at The College of Chicago Sales space College of Enterprise. The conclusions drawn from the NielsenIQ information are these of the researchers and don’t replicate the views of NielsenIQ. NielsenIQ is just not chargeable for, had no position in, and was not concerned in analyzing and getting ready the outcomes reported herein. This analysis didn’t obtain any particular grant from funding companies within the public, business, or not-for-profit sectors.

Creator Word: Wanjia’s contribution to this analysis mission was accomplished upon receiving his Ph.D. in 2022.

Articles characterize the opinions of their writers, not essentially these of the College of Chicago, the Sales space College of Enterprise, or its college.

Originally posted 2023-10-02 10:00:00.