Following up their latest evaluation of danger within the banking system, DeMarzo, Jiang, Krishnamurthy, Matvos, Piskorski and Seru argue that banks must be required to promptly elevate fairness capital so as to scale back fragility and supply a wanted market check to determine really bancrupt banks. They estimate that quantity of personal capital wanted is within the vary of $190 to $400 billion.

The present financial tightening episode has revealed unanticipated fragility within the banking system, narrowing the trail for coverage makers trying to tamp inflation whereas avoiding extra extreme financial dislocation.

From the beginning of the Covid-19 pandemic in March 2020 by way of March 2022, the financial slowdown mixed with financial easing and enormous fiscal transfers elevated whole deposits at business banks by over 30%. This unprecedented progress in financial institution liabilities led to corresponding asset progress, largely within the type of tradable securities together with longer-term treasuries and mortgage-backed securities.

As rates of interest have risen dramatically over the previous 12 months, the market worth of financial institution belongings have fallen. Given the maturity mismatch between financial institution belongings and short-term deposits, the online impact has been an erosion of financial institution solvency. Throughout the banking system, Jiang et al. (2023) estimate the mark-to-market losses on the reported period of bank-held securities and loans alone to be $2 trillion. Whereas a full accounting of those losses has been prevented by banks capability to take care of held-to-maturity belongings at their e book worth, there isn’t any avoiding the financial actuality that the true worth of fairness capital within the banking business has fallen by no less than this quantity.

These reductions are unequally distributed throughout the system, with some banks being significantly onerous hit. Determine 1 plots the distribution of the fairness/asset ratio throughout the 4800 banks within the U.S. banking system. All the distribution shifts to the left from 2022Q1 to the current, based mostly on the Jiang et al. (2023) estimate of marking financial institution belongings to market. 2,315 banks – accounting for $11 trillion of belongings in combination – fall beneath the 0% line in determine 1.

The essential implication of this evaluation is that the latest fragility and collapse of a number of excessive profile banks just isn’t an remoted phenomenon. Practically half of U.S. banks may face related difficulties if compelled to liquidate a major fraction of their belongings within the wake of huge deposit withdrawals.

Determine 1

That stated, the mark-to-market check mirrored in Determine 1 is a element of solvency, however just isn’t determinant. Banks have franchise worth that isn’t mirrored within the worth of the securities and loans they personal. Thus it’s probably that a big fraction of the two,315 banks within the determine are solvent on a long-term foundation even after the rate of interest shock we now have skilled.

The creation of the Financial institution Time period Funding Program along with the implicit extension of deposit insurance coverage to all depositors has put a pause on the disaster and lowered the danger of acute deposit runs throughout the banking system within the brief run.

Narrowly, within the case of SVB and different latest financial institution closures, the federal government’s motion has prevented ethical hazard. The homeowners of the financial institution, whose choices have led to financial institution failure, have been worn out and the financial institution’s belongings will likely be bought to new homeowners.

Nonetheless, the federal government’s actions have amplified ethical hazard for each different financial institution within the system. They’ve implicitly insured non-insured deposits, and the BTFP supplies partially unsecured loans, since these loans are under-collateralized. Lastly, each the low cost window and the FHLB have prolonged loans to banks at beneficiant phrases. The federal government’s total publicity to the banking system has subsequently enormously elevated. Within the close to time period, the banking system’s lowered fairness place can set off a credit score crunch in a repeat of the 2008 monetary disaster, whereas over the longer-term the ethical hazard of the federal government backstop can result in imprudent lending as within the Nineteen Eighties Financial savings and Mortgage disaster.

The essential query going through the Fed and Treasury is subsequently to evaluate the true financial solvency of the banks it’s supporting. The traditional Bagehot dictum of lending freely in opposition to good collateral prescribes offering liquidity to keep away from a run on a solvent financial institution, whereas not offering liquidity to prop-up an bancrupt financial institution. The latter is the achilles heel of presidency backstops, resulting in the issues of ethical hazard, zombie lending, and regulatory forbearance.

How can the federal government keep away from the calamitous path taken all too typically of regulatory forbearance, as within the Financial savings and Mortgage disaster, the Japanese banking disaster, and the European debt disaster?

Financial solvency requires a market check. The flexibility to lift new fairness or long-term unsecured debt from exterior traders is a market check that attracts a clear line between solvent however illiquid and bancrupt. As well as, new capital inflows will scale back fragility and restore “pores and skin within the recreation” for these establishments.

We subsequently suggest the next coverage actions:

- Limit fairness payouts for the foreseeable future. Whereas not a direct market check, this can protect capital inside the banking system and scale back ethical hazard.

- Tie continued entry to authorities lending services, together with the BTFP, the low cost window and the FHLB, to elevated fairness. Inside 90 days of accessing the ability, the financial institution should provoke a capital elevate so as to keep entry to the BTFP.

- Couple all extra assist and regulatory forbearance to a normal enhance in capital necessities for probably the most affected banks.

The fairness elevate is the guts of our proposal. As famous, it’s a market check that identifies really bancrupt banks. The choice to this broad-based fairness elevate are one-off resolutions of failing banks, as the federal government has pursued within the case of SVB, Signature, and First Republic. From our evaluation, the variety of banks at present within the hazard zone numbers within the 1000’s, in order that repeating this strategy is just not possible.

Elevating fairness capital now may also be much less disruptive to the financial system than having a lot of small and medium sized banks fail. Resolving SVB already has required an asset sale on the order of $100 billion. Because the variety of banks on this state of affairs grows, this quantity can simply run into the trillions of {dollars}, and dealing by way of these resolutions can take years as within the S&L disaster.

As we compute subsequent, an fairness elevate proper now would require an infusion of personal capital within the vary of $190 to $400 billion.

We assess the required degree of capital as follows. For every financial institution i, let Di be the overall degree of deposits and FHLB loans. Let kbe the specified degree of protection of those liabilities (“protection ratio”). Given e book belongings Ai, and mark-to-market losses Li, the required extra capital, RCi, for financial institution i is given by

RCi(ok)= max[0, (1+ k) Di- (Ai- Li)]

Observe that when the protection ratio ok is detrimental, the financial institution’s present mark-to-market belongings are inadequate to satisfy its deposit claims and present FHLB loans; that’s, the federal government would incur losses within the occasion of a run.

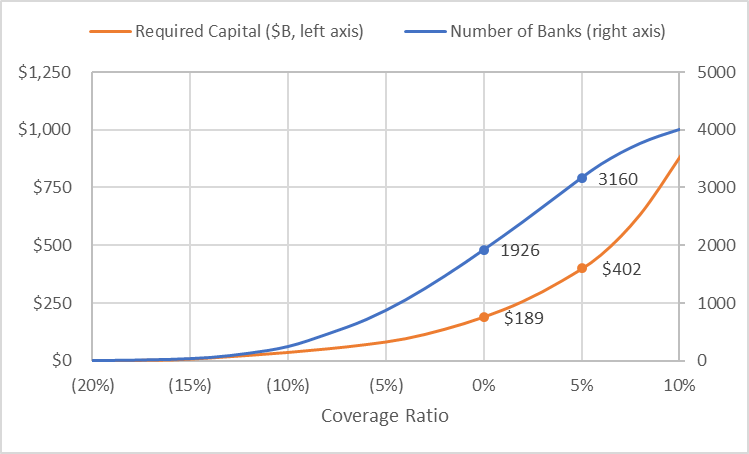

Determine 2

Determine 2 makes use of the identical knowledge as in Jiang et al. (2023) and exhibits the variety of banks beneath every protection ratio ok (i.e. these with RCi(ok)>0). For instance, roughly 1900 banks have a protection ratio beneath zero — the mark-to-market worth of their belongings is beneath the extent of present deposits and government-backed loans. Of these, about 1000 banks have a mark-to-market shortfall (detrimental protection) of greater than 4%. As famous, one-off options as within the case of SVB, Signature, and First Republic should not viable for this variety of banks.

Determine 2 additionally exhibits the overall capital infusion required to revive a given protection degree (the sum of RCi(ok) over all banks). To get all banks above zero would require $189 billion in whole capital, a mean of $98 million per financial institution. Elevating the extent of protection to a modest 5% would require roughly 3200 banks to lift a mean of $127 million every for a complete of roughly $400 billion in new capital.

To supply some context, $189 billion just isn’t a big quantity relative to the accessible provide of danger capital. For instance, the quantity of dry powder within the personal fairness business is over $3 trillion, and certainly the monetary press stories that a few of this capital had been actively evaluating the mortgage e book of SVB. Moreover, the quantity required to enhance a given financial institution’s capital place is far smaller than the quantity required to resolve all the financial institution’s belongings, as would occur in an FDIC financial institution decision. Resolving all of the banks at present within the hazard zone by promoting belongings would require traders to soak up over $2 trillion of belongings.

Reference

Jiang, Erica; Gregor Matvos, Tomasz Piskorski and Amit Seru. 2023. “Financial Tightening and U.S. Financial institution Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?”, Working paper accessible at SSRN: http://dx.doi.org/10.2139/ssrn.4387676

Our proposal requires elevating capital to deal with mark-to-market losses, quite than elevating de jure capital necessities that are accounting based mostly and should still be glad for a lot of troubled banks. (Observe that risk-weighted capital necessities don’t mirror the rate of interest danger inherent in long-term authorities bonds.)

The quantity of capital raised must be assessed by regulators on a bank-by-bank foundation. The end result of this evaluation might be a capital elevating plan, which includes some mixture of revenue retention and new capital.

Why not cease elevating/decrease rates of interest?

The Fed is elevating rates of interest to rein in inflation. The losses within the banking sector are attributable to these actions. But it surely doesn’t comply with that a greater technique could be to surrender on inflation and prioritize avoiding financial institution losses. The price of inflation is commensurate in measurement to the complete $20+ trillion U.S. financial system, whereas our computations point out that the banking sector fragility might be prevented with a capital elevate of some $100 billion.

This straightforward cost-benefit evaluation signifies that coverage ought to guarantee banking sector stability whereas persevering with its concentrate on inflation. Final, this computation additionally signifies that it might be environment friendly for the federal government to place in place extra monetary incentives for banks to lift fairness capital, presumably with authorities investments in most popular fairness.

Avoiding “Stigma”

A voluntary fairness elevate is more likely to be seen as a detrimental sign by the market (as within the case of SVB). To keep away from such a stigma, it is vital that the required fairness elevate be made throughout the board and contingent on typically accessible data. On this means it is not going to present a brand new detrimental sign for the affected banks.

We advise a mark-to-market “stress check” alongside the strains of the essential evaluation described right here to set the brand new capital elevate for particular person banks.

Will requiring an “Fairness Increase” scale back lending?

Our proposed fairness elevate relies on steadiness sheet losses which have already occurred, and so will impose no direct price on new lending. Conversely, by boosting accessible capital, this proposal ought to improve lending capability.

It’s also price noting that elevating customary accounting-based capital necessities would as a substitute be more likely to provoke a credit score crunch by tying new lending exercise to extra capital necessities. This is the reason our proposal emphasizes elevating capital not elevating capital necessities.

Isn’t endurance a greater technique?

Whereas it’s tempting to attend for affected banks to resolve on their very own, there are essential downsides to this strategy:

- Banks stay extraordinarily fragile to deposit losses and depending on authorities assist.

- Given their present debt overhang, banks will discover it enticing to scale back new lending and/or enhance risk-taking, probably exacerbating the disaster.

- Banks that try and resolve the debt overhang on their very own will likely be topic to detrimental stigma results and so could also be reluctant to take action.

- Quite a few regional banks have mortgage publicity to business actual property and may expertise extra stress. That is an asset class that’s more likely to expertise turmoil over the following few years [see this analysis (link)]. It is crucial that regional banks keep robust steadiness sheets to keep away from any systemic danger from the business actual property sector [see this analysis (link)].

Why is a “Market check” wanted?

On a mark-to-market foundation, a lot of banks are technically bancrupt within the sense that their present belongings don’t cowl their excellent liabilities to depositors and government-backed loans. That stated, they might have adequate franchise worth – stemming from their capability to generate future earnings – to rather more than offset this hole. Fairness (or junior collectors) may have the most effective capability and incentive to evaluate the potential franchise worth. These for whom it’s adequate ought to be capable of elevate new capital at cheap phrases.

Conversely, these banks who fail this check are each technically and economically bancrupt. Permitting them to proceed is more likely to exacerbate the issue as they are going to be tempted to tackle extreme danger to “gamble for resurrection” on the authorities’s expense (as occurred within the second stage of the S&L disaster).

Elevating Capital vs Regulation

The choice response to elevating capital is new micro-regulation of financial institution exercise to keep away from the detrimental penalties of debt overhang.

Our strategy is as a substitute to revive satisfactory “pores and skin within the recreation” for solvent banks and extra rapidly resolve these which might be not economically viable. The top consequence will likely be a extra strong and aggressive banking system, avoiding years of potential stagnation and fragility.

Articles characterize the opinions of their writers, not essentially these of the College of Chicago, the Sales space Faculty of Enterprise, or its college.

Originally posted 2023-04-20 10:00:00.